The CU Water Cooler Symposium has always been about more thanjust sharing ideas but actually acting on what you've learned and the connections you've made during the two-day event. Thegoal is for attendees to return home armed, psyched and ready toimplement even just one small change.

|That's what we've tried to do with our CU Water Cooler Symposiumcoverage this year.

|We hope you enjoy this quick video before you head on into themore in-depth coverage of the event held Oct. 4-5 in the FristCenter for the Visual Arts in Nashville, Tenn.

|We also have to give a huge thanks to everyone behind the scenesat the CU Water Cooler Symposium and especially Tim McAlpine,president/creative director at Currency Marketing for all thephotos.

|Have Credit Unions Lost Their Souls?

Have credit unions lost their souls?

|That's just one of the questions Keith Leggett, vice presidentand senior economist at the American Bankers Association, said theindustry as a whole had to consider.

|In his talk to the CU Water Cooler Symposium, he lauded creditunions for their brand of “you belong” but challenged them toreally think about what that means?

|“What is the value of ownership in a credit union?” said Leggettduring his session at the two-day CU Water Cooler Symposium. “Whatis it you get to exercise as an owner outside of voting for a boardof directors? When you look at that ownership stake you can'ttransfer it, can't sell it, can't take it with you. So while yougive a great PR line that you own us I don't see anything beingconcrete with regard to ownership. On top of that do you treat yourmembers as owners?”

|If members were truly owners, he challenged credit unions tovoluntarily disclose a material event, significant loss in loans orregulatory enforcement action.

|“Publicly traded banks have to make these disclosures if theyhave 2,000 shareholders,” said Leggett. “How many credit unionshere have 2,000 or more members? So what happened is that you arereally keeping members in the dark, treating them like mushrooms.So 'you belong' is great PR but you don't go further and treat themlike owners.”

|In a survey conducted by the ABA, while consumers generallytrusted credit unions more than banks and felt like a person ratherthan a number, their perception was also that in terms ofconvenience and access credit unions were “worn rugs rather thanmarble floors,” Leggett said.

|“In an earlier session it was said credit unions had to be theexpertise providers,” said Leggett. “How are you going to becomethat if people perceive you as being the worn rugs, which I took tomean that credit unions don't offer that type of sophisticationthat people would need or would go to get advice.”

|He further suggested that the tax exempt status has actuallybeen holding credit unions back from serving their members moreeffectively in a relevant way.

|“Whenever you have a bank and credit union industry gettogether the conversation always turns to the 800-pound gorilla inthe room: taxation. For our Canadian friends, since 1974 recognizethat it is just part of the cost of doing business,” saidLeggett.

|“CUNA loves to say credit unions are tax exempt because of theircooperative structure, they are democratically controlled and theirvolunteer board members. They cite a finding by Congress from thecredit union membership act however they seem to forget about thisfinding has a conjunction 'and' in there when talking about taxexemption,” he said.

|“It's that you are providing credit and meeting saving needs ofconsumers especially those of modest means. They never want to talkabout that, their social mission,” Leggett said.

|To Leggett, the credit union industry in the U. S. already has aregulatory tax, in the form of limitations.

|“Look at business lending. The is now the fifth Congress in arow where the credit union industry in the U.S. looks to getexpanded business lending authority. Its odds are 98% against thislegislation ever becoming law in this Congress,” said Leggett.

|He suggested the industry has been headed down the same path asthe savings and loans some 60 years ago when they lost their taxexempt status.

|“When you say anyone with a heartbeat can be a member for $10 or$20 'donation', you've lost your souls because it's a movement away from the core value of credit unions. There is no common bond in a $20 bill,” said Leggett.

|“Our view is that the vast majority of credit unions, thesmaller ones in the U.S. should preserve tax exemption because theyare more likely fulfilling their public policy mission. “

|

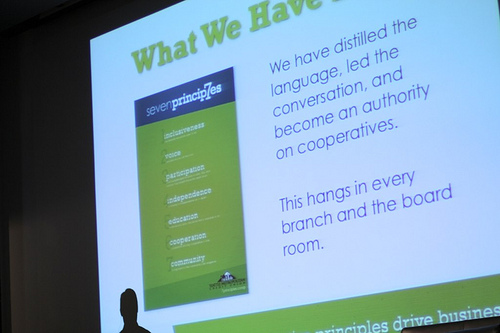

Here are the ways Seattle Metropolitan CU stands out as acooperative authority in the community.

|Now is the Time to Stress the CooperativeDifference

Now is the time to live and play up the cooperative nature ofcredit unions was the message delivered by a few speakers at the CUWater Cooler Symposium.

|Since 2008, Seattle Metropolitan Credit Union has been distinguishingitself from other financial institutions by playing up that it's acooperative.

|According to Andy Wright, assistant vice president of marketingat the Seattle credit union, aligning the culture, marketing andliving the seven cooperative principles has helped grow networksand reach different audiences.

|“It can be a great differentiator but it has to line up withreality. It can't just be something made up by marketing,” saidWright.

|A “Co-opalooza” event, designed to celebrate community andco-ops, has helped build awareness not just of SMCU but also ofco-ops in general. Some 20 co-ops participated in the event whichincluded music and special kids activities.

|“It's helped us communicate in a different space because of weshare the same values,” said Wright. “Just be ready to become thelender of record for other co-ops.”

|Gene Blishen, general manager at Mount Lehman Credit Union inBritish Columbia, said that cooperative spirit can also help smallcredit unions think big.

|“Make the seven cooperative principles a part of your DNA. Everycredit union has a core of people who understand,” said Blishen.“Stand for something, know who you are and understand your history.Be authentic and know your market and members. Dealing with peopleand money gets stressful so you've got to have fun otherwise itbecomes problematic.”

|He added that smaller credit unions need to find moreopportunities to collaborate to create new experiences for oldproducts or even to think more in terms of delivery.

|“The good credit unions do is fragile and must be protected. Youcan mitigate risk by defining your own terms and changing yourperspective,” said Blishen. “Don't be afraid to fail, because thatjust gives you an opportunity to do something in a different way.I'm just a hired gun. A huge element of this understanding of yourmembership is talking to them and listening. You don't always haveto listen to the experts because you've got resident experts.Filter your decisions by using the seven principles and maybeconsider what could be an eighth. Is seven enough? ”

|

Gene Blishen is with Mount Lehman Credit Union in BritishColumbia.

||

Be Young and Free, But Don't Be Cheesy

The generation that grew up watching their parents hanging up ontelemarketers isn't interested in being overtly sold to.

|Two of Currency Marketing's Young & Free spokesters – Austin Chapman and Kylie Keene –shared a few insights into reaching the next generation.

|Forget about youth programs that span from 13 to 25.

|“High schoolers don't want to hang with junior high kids andcollege students don't want to be grouped with high school orjunior high kids,” Chapman said of the one size fits allapproach.

|In addition, mobile is huge said Keene, especially for collegestudents.

|“Our schedules are crazy and the ability to see instantly whereour money is going is most important, but it's got to be easy. Wedon't want to have to jump through hoops so just keep it simple,”said Keene.

|While credit unions still suffer from the perception that it's aplace for parents or grandparents, Keene and Chapman agreed thatthere is hope.

|“If you can get past the noise or the idea that you are justselling to us or trying to scam us, once we understand that thereis a difference we'll share that with our friends,” said Chapman.

|

Games People Play

When Tim McAlpine, president/creative director of Currency Marketingand man behind the Young & Free program, opened the CU WaterCooler Symposium, it was literally game on.

|So this year, the 125 attendees gathered at the Frist Center forthe Visual Arts were issued a gaming challenge for prizes rangingfrom Brent Dixon's new “Cradle to Cradle” album and variety of coolgadgets, to an interactive badge granting access to SXSW.

|The true top prize? Becoming a CU Water Cooler editor, who inaddition to blogging, sharing their daily links of what they'rereading, will have the opportunity to speak at the nextsymposium.

|The true goal? To get people exploring, thinking andnetworking/collaborating in a new way to get things done; basicallyliving the whys behind McAlpine and Matt Davis, director of innovation at Filene Research Institutelaunching the CU Water Cooler and Symposium three years ago.

|For Davis, it was also a great way to demonstrate theopportunity that game thinking presents as a way to engageconsumers and solve problems.

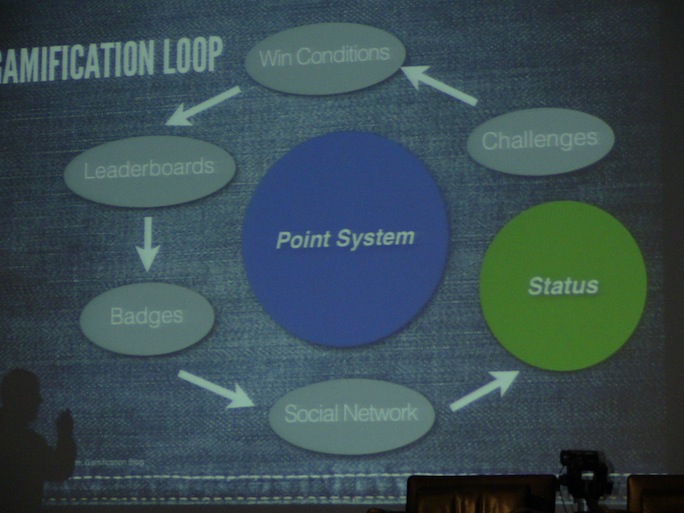

|Looking at the success of Farmville, Weight Watchers, BiggestLoser and Nike+, Davis said it boiled down to an understanding of thegamification loop, which starts with a point system and lettingplayers know what they need to do. From there they are givenchallenges, win conditions, leaderboards to know how they are doingin comparison to others, badges to encourage/reward play and socialnetwork and it all combines and results in status.

|“That's powerful. So a lot of us might have made fun of peoplewho played Farmville but 83 million people played it,” said Davis.“They made a game about farming, which I can tell you, frompersonal experience there is nothing fun about farming. So how cancredit unions use game thinking and fun to apply to financialservices?”

|With credit unions doing a really bad job of capturing people'sattention, Davis said, gamification represents an opportunity todeliver more value to members.

|“If you want to engage members, solve problems, do it by havingfun at the center of it all,” he said.

|According to Davis, it's in the creation of the gamificationflow channel that credit unions have the potential to make the mostimpact.

|“It's the connection between skill and challenge level. So wetry to create solutions in financial services that treat everyoneas if they are at the same level so everyone has the exact sameexperience. The truth is we are all very different, with differentskill levels,” said Davis. In games, at each level the challengesbecome progressively harder because the players skills should beimproving.

|“This is where our head should be at in terms of gamification,”said Davis. “If we can do a better job of matching skill sets withchallenges that are just out of reach, it gets people to workharder to be better and their skill set goes up without them beinganxious or bored.

|“So often the onboarding process is thought of in terms of howcan I get deeper share of wallet. What I suggest to you is to findwhat the skill level is and walk through the description of productand service sign up as a way to understand and maximize the valueof what they are getting.”

|Each task was assigned a range of points, and while for the mostpart honor-based, ultimate verification happened on Twitter. If itwasn't posted, then it didn't happen. During the two-day event, the#cuwcs hashtag was used more than 4,000 times said McAlpine.

|The winners were as follows:

|Team Green won Brent Dixon's new Cradle to Cradle album with3,705 points. With 760 points, Adam Monteith won an Apple TV; 870points landed Rebecca Alcorn a set of Bose in-ear headphones; BlakeReynolds' 1,130 points earned him a Jambone Jambox. With 1,210points Charles Parr will be headed to 2013 SXSW and Amy Etheridgewas the grand prize winner. She had 2,015 points and as a CU WaterCooler editor will speak at the 2013 CU Water Cooler Symposium.

|In addition to Etheridge, with former editors Carla Day,Christopher Morris and Kelley Parks retiring, Matt Monge, RobRutkowski, Shari Storm and CU Times Editor/Publisher Sarah SnellCooke were unveiled as new CU Water Cooler editors.

|

Brent Dixon on Transformation and ThinkingBig

Thinking on a larger scale was the overarching message of BrentDixon's session that kicked off the CU Water Cooler Symposium atthe Frist Center for the Visual Arts in October.

|The Austin, Texas-based founder of The Cooperative Trust shared quite a few facts but the one thatseemed to strike a chord with attendees most was that there aremore payday lenders in the U.S. than Starbucks and McDonald's puttogether.

|In addition, it turns out that one of the top reasons why peoplego to payday lenders is actually in a roundabout way because of thefees.

|The upfront, clearly spelled out charges, even if they arepredatory and making the choice to do so, seems preferable todealing with a financial institution where fees will be snuck in,Dixon said.

|“There's an opportunity to disrupt the current credit unionsystem gatekeepers of Experian, Transunion and Equifax to grantaccess to credit,” Dixon added. “FICO is a really bad riskassessment tool so how do we come up with new models?”

|He pointed to ZestFinance as an example of a new approach to underwriting. Usinglarge-scale, big-data analyzing variables from financialinformation to technology usage has resulted in the ability toextend credit to 25% more Americans, Dixon said.

|He added that the anti-banking industry sentiment has not movedon and that before credit unions laugh thinking it's banks, creditunions are included in that group as people don't distinguishbetween credit unions and banks.

|“Finance, consumer finance can be a transformative tool. Andcredit unions with their structure and philosophy can be a toolbucket in which you can use some of these exponential technologiesand use consumer finance to solve some of the world's biggestchallenges. And that has to be the future of consumer finances,”said Dixon. “Things are broken and we are the people who are calledto fix it.”

|With access to capital as the lubricant to the economy Dixonpointed out that people have come up with new ways of doing thatfrom peer-to-peer lending, which is essentially a technologicaltake on the credit union model, crowdfunding like Kickstarter.comand alternative currency like time and expertise being traded formutual benefit.

|“A friend of mine needed $5,000 to launch his album. He put iton Kickstarter and had a series of goals matched to donationamounts and in one week got $5,000 he didn't have to pay back,”said Dixon. “In New York, alternative currency where say a nursewould give an hour of me being a nurse in exchange for an hour ofyou being a plumber, became so popular they tried to tax it asincome.”

|For Dixon, the World Council of Credit Unions has been a picture of whatdevelopment and transformative work looks like in creditunions.

|“Opportunities exist to increase access. 2.5 billion people areunbanked, there's one simple opportunity to positively impactaccess to credit, savings peace of mind,” he said.

|He added that kind of thinking shouldn't just be limited tounderdeveloped countries and there has been a demonstrated needpresent in developed countries as well.

|Also sorely in need of a large-scale makeover? Collaborationamong credit unions in the U.S.

|“Desjardinsin Canada has helped credit unions claim 40% of market share inQuebec,” said Dixon. “Compare that to our fragmented collaborationin the U.S., which has 6% of market share. There's opportunity todo more. The Occupy movement was a disruptive tool for socialchange. We all want to change something. Credit unions have theability to change something in consumer finance if we act on whatwe say we are built upon. So what does the future of consumerfinance look like? Are credit unions positioned to make it happen?”

|

It's All in the Delivery

Don't be quick to write off humor or underestimate the power ofa joke in telling a story or making a point.

|What if the secret to getting someone as member started with ajoke?

|For Jimmy Marks, creative media director at DigitalMailer insuburban Virginia, the roots of his appreciation for humor sprangfrom the loss of his grandfather when he was a child.

|To help his son smile again, Marks' father told him a pig jokeand he laughed. Fast forward to his first acting gig in “The MusicMan” at 8 years old, one standing ovation later, he was hooked andbecame a student and some would say now, master of humor.

|“Every laugh you've ever laughed, you laughed in the face ofdeath,” said Marks, recognizing that it was a bit of a downer. “Thescariest thing is the door that needs to be opened and the laughsremind us we are alive. It energizes me and gives me a goodfeeling.”

|Some of the simple lessons of humor such as audience iseverything, can also be applied to delivering the credit unionmessage more effectively perhaps with even more authenticity.

|“Timing matters as is recognizing when it is and isn'tappropriate for a joke. In a play you can't be in every scene soyou have to make your scene count,” said Marks. “In improv you'renot allowed to reject what's given to you in a scene. You can'tshoot down an idea you have to build on it. If you can, go to alocal college and have an improv group to teach you something.Humor helps you socialize, remember details of life and makes youaware.”

|Whether it's writing, a project or an idea if it's never sharedor shown to others what good is it? Marks said if no one shows upor responds to it then it wasn't geared to the right audience.

|I would not be standing here if not for Twitter,” said Marks. “Ithink about 60% of the time Facebook is ridiculous and I don't likeLinkedIn or Pinterest but Twitter, that was the place I couldbe goofy. If it runs longer than 140 characters, either write ablog, delete or edit to make it fit.”

|When Joan Rivers started doubting herself and wondered if sheshould change her act because she was a woman and was not widelyaccepted, Bill Cosby advised her not to change because if only 1%ofAmerica loved her she'd fill stadiums for the rest of her life.Marks said the credit union industry and individuals alike canbenefit from that lesson of having the commitment and fearlessnessto stay true to themselves.

|“My heroes were outsiders. Comedians break patterns all thetime,” said Marks. “Dave Chappelle walked away from $50 million tostay true to himself. He's still performing his way without all theroadblocks to doing that. To be a comedian Bill Murray said 'You'vegotta go out there and be completely unafraid to die. You've got tobe able to take a chance to die, and you have to die lots.'”

|The same could be said for credit unions. To be bold enough toidentify their community and the people they want to be in touchwith and vice versa. The same sense of belonging that serves as thefoundation for an inside joke can play into more meaningful,engaged interactions.

|“Funny takes work and sincerity is fuel for the fire. I don'tput anything on Twitter that I didn't want to be there and that ismanicured. There's a lot of stuff I don't put on Twitter,” saidMarks. “Hank Williams said what makes country music so successfulcan be explained in just one word-sincerity. It's the same withhumor, it has to go deep in the gut sincere. It doesn't just fallout of the sky. If you can't be funny, then be sincere. Sinceritywas the reason behind my father telling me that pig joke. He justwanted his son to stop crying. So what if the key to tellingmembers a concise, understandable story that they could connectwith and relate to actually started with a joke?”

||

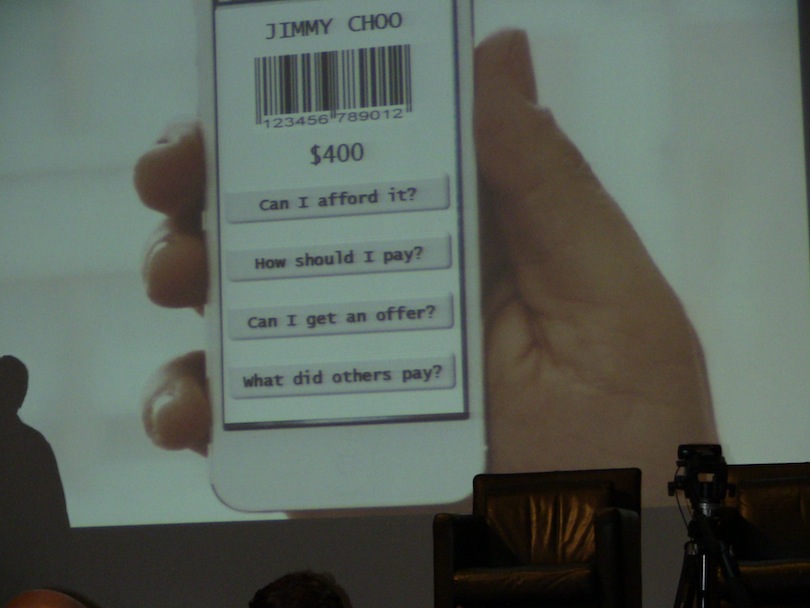

This represents the new moment of opportunity for creditunions to add value with new products and services that membersactually want.

Turn Your Business Model on its Head

Credit unions interested in thriving, distinguishing anddifferentiating themselves in the financial services arena mustturn their current business model on its head.

|“The current business model is dead, dying and you need a newone to reboot for the 21st century,” Ron Shevlin, senioranalyst at the Boston-based Aite Group, told attendees at the CUWater Cooler Symposium.

|He pointed to declining return on equity, which for thefinancial services industry as whole has hovered at about 8% sincedropping from an industry high of 13-15% from 1993-2007. For creditunions in particular there has been a decline in overall grossincome, with revenue falling nearly 4% during a period whenmembership was actually growing.

|“Those are warning signs and growth, cost reduction and pricingchanges aren't going to cut it,” said Shevlin. “I don't thinktoday's business model is going to provide the engine to get usback to historical levels of ROE. We as a society have changed andthe paradox here is as we become a more highly educated, affluent,self-service do-it-yourself, few of us are actively managing ourfinancial lives.”

|According to Shevlin, across the generations three in 10 havesimply not been involved in their financial lives. Gen Y at 33%,turned out to be the most highly engaged in their financial lives,he said.

|He added that over the next few years there will be three bigchanges in the financial services industry: the death of checkingaccounts, separation of production and distribution, and a refocuson financial performance.

|“For the first time in 60 years, it's not a given that whenindividuals reach adult age they will open a checking account.There is a new set of consumers, highly educated consumers who areworking or if they aren't working it's because they are still inschool, choosing to opt out of the traditional banking system,which includes credit unions,” said Shevlin.

|“I call them the debanked. So while you are patting yourselveson the back for the 650,000 consumers who switched during BankTransfer Day, there are 15 million who have left or are aboutleave. There's a need for a new type of account.”

|For example, Movenbank created the concept of CRED as analternative to a FICO score, so consumers have a single accountthat evolves based not on their credit worthiness but debitworthiness. Blending prepaid, credit and debit capabilities, astheir CRED score goes up, customers get additional capabilitiesthat grow with their needs.

|He added that credit unions need to think beyond the old momentsof opportunity under the save and borrow focus such as having a newbaby, or needing a car loan to the new opportunities emerging froma new focus on advise and perform. Given the availability oftechnology and a new more highly engaged generation, the financialservices industry can add more value.

|“We couldn't get to that advice reform of quantifying howconsumers are doing in their financial lives before now,” saidShevlin. “We need to get beyond just personal financial managementto financial performance management. People need to know how muchhave you helped them save and tracking that, how is their moneydoing and what should they do with it? “You have an importantdecision to make: What is your credit union business model going tobe for the 21st century because today's business modelisn't working.”

|Below, Ron Shevlin of Aite Group makes his case at the CUWater Cooler Symposium.

|

Filmmaking Lessons on Leadership

An underlying theme at the CU Water Cooler Symposium waschallenging attendees to think in new ways about common challengesthrough discussions of seemingly disparate concepts.

|William Azaroff, director, business/ communitydevelopment at Vancouver, British Columbia-based Vancity, continued along those lines with leadership tips drawnfrom filmmaking.

|The essence of filmmaking boils down to creativity withinlimits.

|“If you say go innovate, it's paralyzing,” said Azaroff.“Setting that one limitation maybe business model or geographicregion can free up so many ideas so you can innovate to get to whatyour trying to do in your organization.

|“Give people a safe place to take risks and yes there will befailures along the way. You couldn't make a film and not expect tobe bad takes.”

|The difference between films that got made and those that didn'twas the drive of the people involved, Azaroff said. He said hefound that people worked their best on a project they believed in,the same holds true for credit union staffers.

|“Our mission is an advantage. People want to do interesting workand be a part of an organization steeped in mission,” said Azaroff.“People need clear direction you've got to communicate beyond thepage. You always hear 'hire people who are more talented than you.'I say hire those who are differently talented, who offer differentperspectives. Bring creative and tech people together tocollaborate and work to solve problems.”

|Azaroff shared a story about a friend he recently reconnectedwith ho was still pursuing a dream of being a screenwriter aftermore than 10 years of failing.

|“I thought how sad, she's just deluding herself. Then afew years ago, one of her scripts was bought by a really well-knowndirector, and then another got picked up and now she's being hiredto write an original screen play. So what looked to me likedelusion turned out to be persistence. How does the credit unionindustry strike the balance between delusion and persistence?”

|If every story has a villain, then apathy has been the creditunion industry's greatest villain, Azaroff said.

|“Inspiration comes from long slogs. Something that looks easycomes from long thought. I got advice to make the films you want tosee. So what's missing from your marketplace?”

Branding Gives Way to Storytelling Gives Way toWhat?

Forget about branding, storytelling or whatever the nextmarketing trend may be.

|According to David Baker, principal of consulting firm ReCoursesInc., the process has become so watered down that in most casesit's become just a service term geared toward getting money morethan delivering results.

|“Over last five years have you heard more about branding frommarketing firms or farmers,” said Baker to attendees at the CUWater Cooler Symposium. “Have you ever seen farmers brand theircow? Unless your firm or your client smell burning flesh or burninghair and someone is screaming, real branding is not taking place. Ibelieve in a brand but branding as a discipline is dead. Very fewdo it in a way that matters.”

|He added that the brand is important and storytelling may beeven more important as it's emotive and tells the fact in a waythat consumers are more likely to absorb and connect with. but thatonly a few people are investing the time and continuous effort thatgoes into it.

|What matters most is for credit unions to think of themselves asnot being in the service business but rather the expertisebusiness, Baker said.

|“There are three dry cleaners in my neighborhood and if my drycleaner ticks me off then I'll just go to the drycleaner around thecorner. The point is that the only time I care about or noticethose in the service business is when they screw up,” said Baker.“If you are in the expertise business that means you are as aninstitution doing what's right for the consumer even if it meansyou don't make as much money. So members aren't headed to yourcredit union just to park their money but because they need answersto something that's important to them.”

|One way for that shift to happen starts with having people inthe organization who believe in and live the mission.

|“With all the homogenous offerings how can financialinstitutions get back to thinking differently aboutspecialization?” Baker asked. “You want to change the world?Start first with your significant other, next your children, thenfriends and fourth the people you manage. Very few of us have ahuge platform but change how you manage your people and you'll findthat those people do a much better job of representing your creditunion than any marketing.”

|He added that educating consumers in financial literacy is agood start to being in the expertise business as most consumersstill aren't able to navigate their finances.

|

Marketing to Technology: Let's Get Together

Why can't marketing and technology not only get along but worktogether to solve common consumer concerns?

|According to Ed Brett, manager, product and service delivery at BritishColumbia-based Westminster Savings Credit Union, it's past time toleverage the strengths of both departments to do more formembers.

|“We need to be sensitive to the way technology is changing our relevance to members,” said Brett. “Alternative lendingcompanies and increasingly media and technology companies arebecoming more relevant to the day–to-day financial lives toconsumers than we are. Instead of coming to us members move to themfor answers on their financial lives. Why does Suze Orman have moreinfluence in our members' lives than our branch managers?”

|Brett added that a more symbiotic relationship between IT andmarketing departments could help make a real difference. As anexample, he pointed to the uselessness of personal financialmanagement as a standalone platform.

|“We asked consumers where did you learn how to manage yourfinances and we thought we'd hear answers like from my parents orfinancial literacy initiatives but what we actually heard was 'I just had to figure it out on my own,' which meant that theyweren't managing their finances at all,” said Brett.

|“The value for us here is how to take technology like PFM to addmore relevance and value to members' lives,” he said. “We havepeople in branches who can deliver value through technology toothers, we have principles and we can own that. Our stakeholdersare the people we serve and this represents an opportunity for usto provide a service they really need, using PFM tools for example,based on why it matters and is important to them.”

|He added that IT has been an untapped, underutilized resourceand looking ahead there should more of an effort to includetechnologists in the strategic process.

|“Technology should be as involved with upstream decisions asthey are with the downstream implementation,” said Brett. “Havethem be a part of the discussions and let them take responsibilityfor the growth strategy in your credit union and be as creativeabout your credit union as your systems.”

|The common challenge with technology and banking has been how totake those concepts that exist as abstracts and make them real.

|“The most important part of the Amazon experience for me is notwhat occurs at the point of purchase but what happens seven dayslater. There's the package and it's Christmas or my birthdayagain,” said Brett. “When I was in IT the things that mattered tothe organization were abstractions to me especially our members.Two days in the call center cured me. The cool things I wascreating didn't matter at all to all these people calling inbecause it didn't help them. “In general, IT is disconnected fromthat conversation and that is a risk for your credit union. It'sdangerous to have your IT group treat your members as abstractionsas well. “

|He advised marketers to be excellent observers of the littlethings.

|“Look for ways that members actually use the technology ratherthan how you want them to,” said Brett. “How you want them to havea relationship with you is not up to you anymore, so you have tostart paying attention to what really matters.”

|

Andy Janning of No Net Solutions makes his point to the CUWatercooler crowd.

Creating Workplace Heroes

To truly build better organizations, focus on helping othersevolve.

|That was the underlying message delivered by Matt Monge, chief culture officer at Mazuma Credit Union, andAndy Janning, president/CEO of No Net Solutions, during the CUWater Cooler Symposium.

|“We can't think of employee development as exclusive to adepartment or one person, “ said Monge. “It has to be more than that. It has to be theorganization's way of life, be baked into the culture that it is acommunity effort on the part of everyone there.

|“If you don't do that and reduce it to just a department you'llhave at best mediocre development of folks.”

|Janning added that every employee is a hero to someone and thereis nobility in helping someone evolve.

|“We've got to completely rethink the role of people in employeedevelopment, it's not an exact science and is designed to beimperfect. The way it's done now implies an endpoint, which doesn'texist,” said Janning.“Every hero story ever told on earth, there is always a trainerfigure, always a point where the hero messes up. Each of you areexperts in something. Each one of you can make someone elsebetter.”

|He said it's the job of the organization to pay attention tohelping the employees, who essentially hold up the walls of creditunions, evolve and to make those subject matter experts shine.

|Monge added that it's time to stop holding the trainingdepartment more accountable for employee development than theirmanagers.

|“Sending employees to a training session, a conference or evensending them a link to an article is not developing them,” saidMonge. “What if we make it not OK for leaders not to lead theirpeople by asking them what specifically have you done to helpdevelop their dreams?”

|He added that development is not just for front-lineemployees.

|“Consider the fact that if employees are not seeking it out, notgrowing, it could be because they don't see any of us doing it. Thediscussion they usually have is, 'Here sign this paper that we hada conversation,'” said Monge. “We've got to be doing better thanthat. They should see their managers go out to pursue their owndevelopment and be modeling that learning and growing never ends.We have to stop this idea where employee development is teachingfront line staff.”

|The academia model of studying to pass a test cannot be appliedeffectively in helping employees evolve in the workplace, thespeakers said.

|“No one ever learned to ride a bike in a workshop,” saidJanning. “Knowledge is not power. Performance is power. We need tostop making knowledge something that only the gatekeepers of anorganization have. People go to programs for one goal paycheckimprovement.

|“They want to do more so they can go home whole, healthy, happyand be the hero to the people who greet them at the door. The spaceorganizations need to be in is to help employees evolve through KPP– knowledge, practice and performance.

|“To screw up safely is part of the job, not to pass the test butpractice effectively and measure performance. We can each makesomeone better. It starts with how are we developing employees? Howare we making them heroes?”

|Below, Matt Monge of Mazuma Credit Union says employeedevelopment must cross departmental lines.

|

Complete your profile to continue reading and get FREE access to CUTimes.com, part of your ALM digital membership.

Your access to unlimited CUTimes.com content isn’t changing.

Once you are an ALM digital member, you’ll receive:

- Critical CUTimes.com information including comprehensive product and service provider listings via the Marketplace Directory, CU Careers, resources from industry leaders, webcasts, and breaking news, analysis and more with our informative Newsletters.

- Exclusive discounts on ALM and CU Times events.

- Access to other award-winning ALM websites including Law.com and GlobeSt.com.

Already have an account? Sign In

© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.

link")