Around 16 million new U.S. households – many of themdiverse – are expected to emerge over the next decade, bringingcredit unions and banks big mortgage lending opportunities,industry experts said.

Around 16 million new U.S. households – many of themdiverse – are expected to emerge over the next decade, bringingcredit unions and banks big mortgage lending opportunities,industry experts said.

“We need to remember the low rates of household growth we haveseen in the last five years have not been usual,” Mortgage BankersAssociation Vice President of Research and Economics Lynn Fishersaid in an interview about the expected growth wave.

|The Great Recession slowed new household growth and expandedexisting households' sizes because fewer jobs prevented youngpeople from moving out of family homes, Fisher explained. It alsoforced families to move in together due to foreclosure or to savemoney, she added.

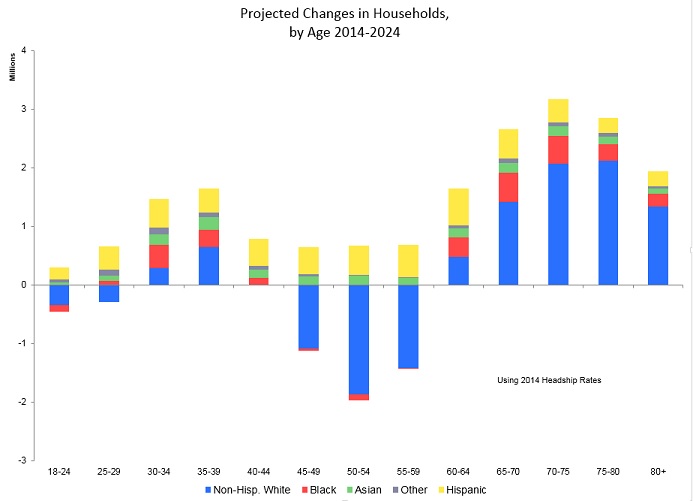

|However, as jobs continue to grow and existing householdsundergo life changes, Fisher forecasted as many as 16 millionadditional households by 2024 in all age categories. However, shesaid the growth won't be similar to historic household growthperiods.

|The Washington-based MBA used U.S. Census Bureau data to makeseveral predictions.

|First, baby boomers will lead a new housing wave.

|“Housing demand for age-appropriate housing will increase among[boomers] as compared to the amount of 70-year-old appropriatehousing available in 2014,” she said.

|Second, millennials will add 5.1 million new households withmembers aged 18 to 44 by 2024, Fisher forecasted.

|Immigrants and minorities will also drive household growth. By2024, Fisher said, there will be 5.7 million more Hispanichouseholds, 2.4 million more African-American households and 1.9million more Asian households compared to 2014.

|“Averaging 1.6 million additional households per year, housingmarket growth over the next decade would be among the strongest theU.S. has ever seen,” Fisher wrote in “Housing Demand,” ademographic white paper she published in August 2015 with JamieWoodwell, the MBA's vice president of commercial/multifamilyresearch.

|Fisher observed more households won't necessarily translate tomore homeowners, but said dynamics within each age group makehomeownership growth likely.

|For example, homeownership becomes more likely with age, Fishersaid. The well-documented trend of millennials delaying startingfamilies favors their entry into the purchase market sometime inthe next decade, she noted.

|Robert Dorsa, president of the American Credit Union MortgageAssociation, said he agreed with the MBA's numbers, particularlythose on minority and immigrant household growth. He also saidcredit unions must continue to build trust and create mortgage loanawareness among members to help fulfill the increasing demand formortgage loans.

|“I believe maintaining a high degree of trust with the membersand creating and offering loan programs that appeal to all levelsof consumers and household foundations are key,” Dorsa said.

||“Credit unions are community lenders for the most part. If a fewin the community are aware that credit unions not only exist toprovide a free checking account but are trustworthy institutionscapable of providing quality mortgage loans, we have a chance ofnot only holding on to our almost 10% market share but seeinggrowth. Promoting the credit union story at the local level is atthe heart of any successful growth path in my opinion.”

|Dorsa also emphasized strengthening consumer awareness of creditunions as cooperatives.

|“As you know I have literally grown up in the credit unionsystem,” Dorsa said. “After 40 years observing the 'unknown andmysterious' feeling consumers get when the term credit union ismentioned, I believe it is on us to remove this dark cloud. I stillstrongly believe using or adding the term 'cooperative' in thecredit union's name or branding may be the spark that creates highgrowth. On the other hand, conducting business as we do now couldbe the recipe for little or no growth. If that is the case, even Ido not see much optimism for our brand of banking.”

|Ron Shevlin, director of research for the Scottsdale,Ariz.-based financial institution consulting firm CornerstoneAdvisors, said while he has not seen the MBA's analysis, itresonated with forecasts he saw that pointed to household growth ofeight million in the next five years.

|He also said the new households will reside in purchased homesrather than in rented apartments or houses. But, he conceded thatfor every data point that supports strong future homeownership formillennials, there could be two data points that support a counterargument.

|“The real problem is with our ability to research any of this ina very meaningful way,” Shevlin commented. “It's just verydifficult to ask a 25-year-old what they are going to want in fiveor 10 years. Right now, when you're 25, single and work close towhere you live or in an urban area with good public transportation,it's easy to say I don't need to buy a car or house. But in a fewyears, after they start a family and priorities shift, theydiscover they really do need a car and a house.”

|Like Dorsa, Shevlin urged credit unions to keep building trustwith members, adding they should incorporate mortgage education andspecialize in helping first-time buyers.

|He also reported 30% of millennial credit union members whoconsidered taking out a mortgage loan received education about theprocess, compared to only 15% of non-credit union membermillennials.

|“Becoming known as place with reliable, trusted informationabout mortgage options and getting a mortgage could be a realdifferentiator for credit unions in a crowded market,” Shevlinsaid.

|Credit unions looking to take advantage of household growthmight also find a new Fannie Mae program helpful.

|Dubbed the HomeReady Mortgage, the new program combinesprospective homeowner education with significantly changedunderwriting criteria to benefit both lenders and borrowers,according to Fannie Mae.

|Lender advantages include tying the program into Fannie Mae'ssoftware, allowing the software to automatically identifypotentially eligible loans, the Washington-basedgovernment-sponsored enterprise said in a Sept. 29 announcement.HomeReady loans also carry improved and simplified pricing, and areeasier to sell to the secondary market, Fannie Mae said.

|Borrower advantages include the potential for 3% down payments.Underwriters are also allowed to include income from members ofnon-borrower households when calculating debt to income ratios. Theloans will also allow for non-occupant borrowers and permitunderwriters to include rental income from an accessory dwellingsuch as a basement apartment and boarders, Fannie Mae said.

Complete your profile to continue reading and get FREE access to CUTimes.com, part of your ALM digital membership.

Your access to unlimited CUTimes.com content isn’t changing.

Once you are an ALM digital member, you’ll receive:

- Critical CUTimes.com information including comprehensive product and service provider listings via the Marketplace Directory, CU Careers, resources from industry leaders, webcasts, and breaking news, analysis and more with our informative Newsletters.

- Exclusive discounts on ALM and CU Times events.

- Access to other award-winning ALM websites including Law.com and GlobeSt.com.

Already have an account? Sign In

© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.