Charles Spilman knows that baby boomer generation membersconstitute almost half the share certificate and mortgage businessat United Federal Credit Union in St. Joseph, Mich. But Spilman,director of product planning and card services at the $1.8 billioninstitution, has no intention of creating a separate portfolio ofproducts and services for his boomer members.

|“We've been designing and offering products for boomers fordecades, but we don't specifically target boomers with programs,”Spilman said. “Our approach has been to meet the needs of eachindividual member by having a broad range of products.”

|As the aging demographic enters retirement, baby boomers stillcarry a significant amount of financial clout. Boomers as a groupearn an estimated $2.4 trillion annually that accounts for 42% ofall after-tax income, according to the U.S. Bureau of LaborStatistics' Consumer Expenditure Survey. Experts say that boomersare and will remain a financially significant – and a significantlylarge – age cohort for the next 30 years.

|Despite the fact that the generation born between 1946 and 1964is financially active, credit unions caught up in the media buzzover courting Gen X, millennial and even centennial generationmembers may not be fully tapping the financial resources theyalready have in hand. Because of that, the performance of servicesfor some of credit unions' most loyal and economically viablemembers may be suffering.

|Many credit unions are addressing boomer needs, but some of themost effective programs avoid AARP-like menus of specially designedservices in favor of taking a tightly targeted, yet fullyintegrated approach to serving the age cohort, according to BillCheney, president/CEO of the $11.4 billion SchoolsFirst FederalCredit Union in Santa Ana, Calif.

|“Understanding each member's needs and situation and providingthem expert financial guidance is our best strategy for servingthem,” Cheney said.

|Statistics show that, in some cases, boomers need all thefinancial advice and service they can get.

|As a generation, baby boomers are at a turning point in theirfinancial and social lives as they face and, at an increasinglevel, embrace retirement. But unlike their parents' generation,which was steeped in the deprivation and sacrifice of the GreatDepression and World War II, boomers have spent more and saved lessin preparation for their golden years.

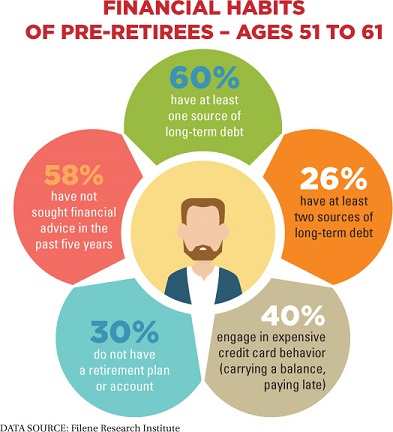

|According to a 2014 Filene Research Institute study, “FinancialCapability Near Retirement: A Profile of Pre-Retirees,” boomers asa generation are characterized by risky spending behaviors, highdebt loads and financial illiteracy, activities that in many casesput boomer members at risk for financial instability that may delaytheir retirement years. The implication for credit unions, thereport said, is a need for more pre-retirement financial counselingand planning to help boomers better cope with financial demands inthe years to come.

|But those same conditions have also produced a generation that'smore robust and creative in navigating its retirement path. Manyboomers are delaying retirement, or abandoning the idea completelybased either on financial or personal needs. Generallywell-educated and healthier than previous generations, boomers areanticipating longer lives than their parents did and adjustingtheir financial activities to accommodate those extra years.

|From a financial activity standpoint, this means continuedsavings and borrowing activity with an eye toward both wealthaccumulation and lifestyle enhancement, experts have said. Plainlyput, boomers will keep on spending and, with an aggregate overallwealth estimated to be in the trillions of dollars, credit unionscan better serve those members by providing integrated financialproducts that actively address boomers' financial needs andpersonal objectives.

|But at least some of those products should also take intoaccount retirement and end-of-life needs, according to EricHansing, vice president of life, AD&D and media for CUNAMutual's TruStage product line.

|“According to research, 62% of boomers say they worry abouttheir financial stability every day, but are proud of the fact thatthey can still make ends meet,” Hansing said. “But in terms ofpreparedness for retirement, I'd give them a C+.”

|Personal goals and objectives matter greatly for boomers,according to “What Matters Now: Insights from the Middle,” aTruStage research study that explored middle class segments ofmultiple demographic groups. Survey results showed that boomersshared many values with other demographic groups.

|Raising children to become good adults and having a good spousalrelationship ranked highest among the two million consumersTruStage surveyed. Having enough money to be financially stable andstaying in good health tied for third place, while a strongrelationship with a higher power rounded out the top fivegoals.

|Each of the five goals comes with its own challenges, butfinancial security is one in which boomers can take specific stepstoward success, Hansing said.

|“Saving for retirement is a big deal, and the shocks that cancome from loss of job or healthcare expenses can be hugedisruptors,” Hansing explained. “Insurance products that providefinancial support in the face of health issues and death are thecenter of the bullseye.”

|| For many boomers, that means a return to traditional,whole life insurance policies that provide a significant deathbenefit, Hansing said. Boomers also like to buy whole life policiesas gifts for grandchildren so they have some level of insuranceprotection as they mature.

For many boomers, that means a return to traditional,whole life insurance policies that provide a significant deathbenefit, Hansing said. Boomers also like to buy whole life policiesas gifts for grandchildren so they have some level of insuranceprotection as they mature.

In addition, CUNA Mutual offers health insurance and a varietyof other coverage through TruStage, but the Madison, Wis.-basedinsurer has stopped offering long term care coverage, CUNA Mutualspokesman Phil Tschudy said. Lack of demand may have led to thedeletion of this business line, he added.

|TruStage currently serves the insurance needs of more than 4,000credit unions and their members, bringing additional advantages tothese individual institutions, Hansing said.

|“The three areas on which boomers get stuck when it comes tolife insurance are assumptions about affordability, understandingpolicy intricacies and concerns that insurance is hard to get,”Hansing explained. “Credit unions that get behind TruStage programssee more of their members protected, while letting us do all thepromotion and work.”

|At United FCU, insurance certainly plays a role, along with amore holistic approach that addresses individual needs of boomermembers, Spilman said. It's necessary, he added, because thedemographic itself is fragmented.

|“The boomer cohort is so large that there are multiple segmentswithin it with very different financial needs, and boomers continueto change the rules of the game as they have almost from theirstart,” Spilman said. “It used to be true that as a generationaged, it became less likely to need a mortgage. Boomers have brokenthat trend, partly because they are working longer and are moremobile, but also because they desire to trade up and/or purchasesecond homes.”

|Boomers make up just 31% of United FCU's membership, yet theyhold 49% of share certificates and mortgages, Spilman noted. Theyalso hold 39% of total loan balances and 51% of total deposits,making them a viable and highly active member segment.

|“We take a needs-based approach to sales at UFCU, so we don'ttarget any products specifically to boomers,” Spilman said.

|The numbers are similar, and so is the strategy at $178 millionChaco Credit Union in Hamilton, Ohio. Boomers comprise 31% of thecommunity credit union's membership base and hold 40% of the creditunion's total assets, according to Chaco CU President/CEO JimSchultheiss.

|“Boomers are very financially active,” Schultheiss said. “Theyuse an average of 2.44 services per household, have an average of$10,000 in loans, not counting mortgages, and have a longconnection to the credit union.”

|Like other credit unions, Chaco CU does not isolate a list ofservices specifically tailored toward boomers. Instead, Schultheisssaid, member service representatives are trained to isolate andaddress individual financial needs specific to individual members'situations, providing service at as many levels as possible.

|“We believe in serving each member as an individual, thus feelall of our marketing of individual products is specific,”Schultheiss explained. “Our focus on providing sound information,as opposed to strong bank sales tactics, has been very successfulin the baby boomer demographic and as a whole.”

|SchoolsFirst FCU's Cheney would agree with Chaco's approach.Although the credit union doesn't measure individual memberprofitability, Cheney knows that boomers comprise 26% of theeducational credit union's 651,000 members, and as such are afinancial force to be reckoned with.

|“Baby boomers are experiencing a wide range of life events, frommeeting the needs of teenage children, to sending their children tocollege, planning for retirement, or enjoying retirement,” Cheneysaid. “Our role is not to put them in broad segments, but insteadto understand them individually and ensure our products andservices meet their unique needs, with the goal of bettering theirfinancial lives.”

|Bucking trends has been the hallmark of baby boomer culture fromthe beginning, and serving nontraditional personalities with anontraditional approach to financial products is critical forcontinued success, Cheney said.

|“We serve our baby boomer members today and will continue tounderstand their needs now and in the future,” he added.

Complete your profile to continue reading and get FREE access to CUTimes.com, part of your ALM digital membership.

Your access to unlimited CUTimes.com content isn’t changing.

Once you are an ALM digital member, you’ll receive:

- Critical CUTimes.com information including comprehensive product and service provider listings via the Marketplace Directory, CU Careers, resources from industry leaders, webcasts, and breaking news, analysis and more with our informative Newsletters.

- Exclusive discounts on ALM and CU Times events.

- Access to other award-winning ALM websites including Law.com and GlobeSt.com.

Already have an account? Sign In

© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.