Industry experts say due diligence can help credit unions avoidlosses like those suffered by the $620 million Alabama One CreditUnion in Tuscaloosa, Ala., and the Small Business Administration,which were defrauded of more than $3 million by a businessman.

|Danny Ray Butler allegedly engaged in a check-kiting scheme thatled to a $1.275 million loss at Alabama One. He also allegedlydefrauded the SBA of $1.76 million through a loan to build a grocery store,according to a 51-count indictment and statements made Oct. 4 byU.S. Attorney Joyce White and FBI Special Agent in Charge RichardD. Schwein Jr., in Birmingham, Ala.

|Butler was likely able to get away with the alleged check kitingscheme because he was well known in the community and had probablybuilt a level of trust with the financial institutions involved,said Kent Moon, president/CEO of Member Business Lending LLC, a WestJordan-based CUSO.

|Moon, who has nearly 40 years of experience in the small business lending sector, once served as district directorof the SBA's Utah district and as a financial analyst and seniortechnical adviser for the agency's headquarters in Washington.During that time, he said he worked closely with the Department ofJustice and the FBI in assisting with the prosecution of thousandsof embezzlement and check kiting cases.

|“The thing I learned is the people who are involved aretypically normal, everyday people,” Moon said. “They're not goingto come across as the criminal type or the Hollywood version ofwhat that is. Usually, the chief suspects have built a high trustcapacity in the community.”

|For credit unions and other financial institutions, check kitingfraud is estimated to run into the billions of dollars in losseseach year, according to some industry data. Even though check useis declining, the U.S. Treasury's Financial Crimes EnforcementNetwork found that check fraud has become the second most commoncrime reported in suspicious activity reports behind moneylaundering. Of the more than 50,000 SARs filed by depositoryinstitutions in 2010, the latest year tracked by FinCEN, theaverage suspicious activity amount was $766,270 and the averageloss amount was $18,836.

|With small businesses, check kiting typically occurs when theowner is experiencing a personal crisis such as a divorce or adeath in the family, Moon said. The irony is the perpetratordoesn't think he or she is actually stealing, he explained.Instead, the business owner believes he or she is borrowing themoney, and has every intention of paying it back.

|“It's hard to protect yourself from someone you trust,” Moonsaid. “This happens more frequently than people realize. I'm alwaysamazed at how many businesses and financial institutions getnailed.”

|For credit unions, check kiting protection goes back to thebasics, Moon noted. There must be strong procedures in place forcash verification. When surprise verifications occur, the businessowner doesn't know when the accounts will be checked, which givesthe financial institutions more time to follow the trail, hesaid.

|Other red flags credit unions need to watch for are deposits ofincreasing dollar amounts and frequent returns of unpaid checks,said Ken Otsuka, senior consultant, risk management at CUNA MutualGroup in Madison, Wis.

|Over the years, Otsuka said he has seen new account fraud caseswhere the culprit pretends to be a business owner, opens an accountat a credit union, starts making deposits and then withdrawals thefunds. There have also been cases involving dishonest employees whoopen an account in the name of the business without the authorityto do so, Otsuka noted. The employee can then embezzle those fundsfrom the business.

|“Luckily, we don't see many of these cases,” Otsuka said. “Whenit does happen, the losses can be very severe.”

|Next Page: Specific WrittenPolicies

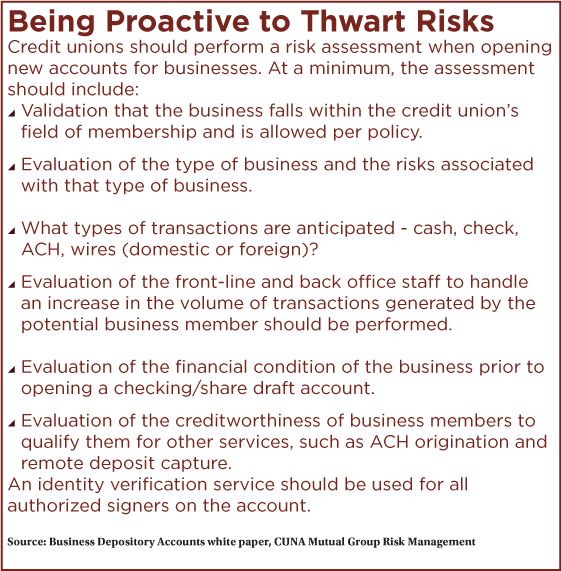

||Otsuka said he is a firm believer in business members qualifyingfor certain products such as remote deposit capture and ACH origination. Written policiesshould specify the type of businesses a credit union wishes toattract and identify undesirable businesses, he suggested. Duediligence should always include evaluating a business's financialcondition and requesting updated financial statements and taxreturns on an annual basis to help detect any negative changes in abusiness member's life.

|In their efforts to attract more businesses, some credit unionsare offering RDC. Unfortunately, the remote service can help abusiness member maintain his or her check kiting scheme, especiallyif a credit union employee doesn't review the check image, Otsukasaid. By qualifying members for RDC based on their financialcondition and requiring annual checkups of financials, creditunions can spot any downward trends.

|“We are seeing a trend with credit unions wanting to expandtheir fields of membership to attract business accounts or increasetheir service offerings to existing business members,” Otsuka said.“Regardless of where credit unions are at, an important startingpoint is having a policy that addresses businesses they want toavoid.”

|For instance, while Otsuka doesn't want to suggest businessessuch as check cashing stores increase risk, they have a tendency toattract fraudsters who might use them to launder stolen money, hesaid.

|When it comes to check kiting, frontline staff may find itdifficult to track suspicious activity because a business could bedepositing high volume of checks and tellers may not have the timeto check through all of them, Otsuka said. In these cases, tellerscan look at the drawer's signature on the face of the check todetermine if it belongs to the business member or an authorizedsigner.

|In 2010, Butler contacted West Alabama Bank and Trust for a $5million loan to build a grocery store, according to the indictment.He received bank approval for half the amount of the loan with theSBA agreeing to finance 35% of the project and Butler providing theremaining 15%. However, after construction was completed, Butlerdefaulted on the bank and SBA loan. It was discovered that Butlersubmitted false, forged and altered documents to get the SBA loan,according to the indictment.

|In 2011 and 2012, Butler was allegedly involved in acheck-kiting scheme that carefully timed deposits and checksbetween his grocery store account at West Alabama Bank and Trustand his Butler Wholesale account at Alabama One to artificiallyinflate the account balances, the indictment read. Checks totalingapproximately $45 million were deposited from one account to theother at the two financial institutions.

|Alabama One and the SBA did not respond to requests forcomment.

|According to the indictment, Butler was also allegedly involvedin another scheme involving securing loans from NextGear Capital, aCarmel, Ind.-based financing company, to buy used vehicles for hiscar lot. He allegedly represented cars that were part of thedealership's inventory even though the cars were already sold.

|Moon said based on what he read about the details in Butler'scase, he secured a 504 loan from the SBA and needed to come up with$750,000 in cash. He started at a bank, then went over to thecredit union and floated cash to give the appearance ofliquidity.

|“Any time you have a borrower using money to build a buildingand he's working with another financial institution, there shouldbe verification of those balances with the other financialinstitution,” Moon said.

Complete your profile to continue reading and get FREE access to CUTimes.com, part of your ALM digital membership.

Your access to unlimited CUTimes.com content isn’t changing.

Once you are an ALM digital member, you’ll receive:

- Critical CUTimes.com information including comprehensive product and service provider listings via the Marketplace Directory, CU Careers, resources from industry leaders, webcasts, and breaking news, analysis and more with our informative Newsletters.

- Exclusive discounts on ALM and CU Times events.

- Access to other award-winning ALM websites including Law.com and GlobeSt.com.

Already have an account? Sign In

© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.