More dealership alliances, better marketing, lower rates or acombination of all three?

|These may be among the factors that have helped some of theindustry's largest credit unions, notably those in thebillion-dollar asset range, to become frontrunners in the autolending sector.

|The data clearly shows which cooperatives are leading the pack.According to CUNA Mutual Group's March “Credit Union TrendsReport,” credit unions with assets ranging from $404 million to$52.4 billion accounted for 80% of vehicle loan growth in 2012.

|Forty-nine percent of credit unions reported positive vehicleloan growth and the 510 largest credit unions by asset sizeaccounted for 80% of 2012's gain, the report's data showed. The 197billion-dollar credit unions also accounted for 57.9% of thatgrowth. On the other end, a total of 145 credit unions in the 510large credit union category group reported declines in their autoloan portfolios.

|Among the factors that have led to strong auto loan activity are the robust sales of stronger, new lightvehicles, less generous financing incentives from captives andlower rates at credit unions, noted the report, which tracked datathrough January.

|“The nation's credit unions are helping consumers and memberslead the recovery. Record mortgage refinances improved memberhousehold cash flow and falling vehicle loan rates helped makevehicle replacement more affordable,” said Dave Colby, CUNA Mutual chief economist.

|Another sign that consumers may be more willing to shop againcan be seen in new vehicle loan originations. The $6 billion gainin new vehicle loans accounted for 22% of all credit union loangrowth during 2012, according to the trends report. Indeed, newvehicle loan rates were down almost 0.5% over the past year to3.41%. The 8.9% gain in used vehicle loans is the best performance since early 2004,the report noted.

|Meanwhile, there's more evidence that larger credit unions arebringing in the bulk of auto loans.

|Competing with some of the nation's biggest banks, five of themrecently made the list for the 25 largest auto lenders amongdepository institutions in the United States.

|

According to SNL Financial, the $15 billion PentagonFederal Credit Union, which ranked 22nd, posted the highestquarterly growth rate in auto loans among the top 25 for the fourth quarter in 2012. TheAlexandria, Va.-based cooperative grew its portfolio by 10.9%during that period by pricing its loans very competitively, thedata showed.

|“Not including any current rate specials, Pentagon Fed's averagerate on a 60-month new car loan was 2.74% as of SNL's most recentrate collection date, significantly below the national average rateof 4.24%,” according to Charlottesville, Va.-based data andanalytic firm SNL Financial.

|Other credit unions that made the top 25 auto lender list werethe $52 billion Navy Federal Credit Union in Vienna, Va., which ranked 14th, $6billion Security Service Federal Credit Union in San Antonio, (No. 17),$5 billion Alaska USA Federal Credit Union in Anchorage, Alaska (No. 23)and the $5 billion America First Federal Credit Union in Riverdale, Utah (No.25).

|Auto loans amassed during the fourth quarter were $691 millionat Navy Federal, $520 million at Security Service FCU, $271 millionat Pentagon FCU, $224 million at Alaska USA FCU and $170 million atAmerica First FCU.

|According to SNL Financial, Ally Financial Inc. in Detroitranked first in its top 25 list of the top auto lenders followed byWells Fargo & Co. in San Francisco, JPMorgan Chase & Co. inNew York, Capital One Financial Corp. in McClean, Va., and Bank ofAmerica Corp. in Charlotte, N.C.

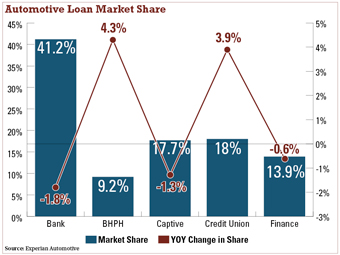

|Regardless of the asset size or whether the financialinstitution was a credit union, bank or other lender, lowerinterest rates and longer loan terms made it easier for consumersto finance a vehicle in fourth-quarter 2012, according to ExperianAutomotive. Average loan terms for a new vehicle during those three months jumped to an all-timehigh of 65 months, up from 63 months in fourth-quarter 2011.

|Experian's fourth-quarter state of the automotive finance marketreport also showed that the average loan amount for a new vehiclewas $26,691 in fourth-quarter 2012, up $272 from the same quarterin 2011, while the average used vehicle loan was $17,629 in 2012, up $239 from 2011, bothin the fourth quarter of those years.

|While consumers are taking out larger loans, lower interestrates and longer loan terms for new vehicles helped bring down theaverage monthly payments. Experian said the average monthly paymentfor a new vehicle dropped in the fourth-quarters, from $468 in 2011to $460 in 2012.

|The average interest rate for a new vehicle loan in 2012 droppedto 4.36%, from 4.52% in 2011. The average interest rate for a usedvehicle loan dropped to 8.48%, from 8.67% during the same period.

|“Lower interest rates and longer loan terms made it easier forconsumers to finance a vehicle while keeping their paymentsaffordable,” said Melinda Zabritski, director of automotive credit for ExperianAutomotive. “This, combined with the fact that more vehicle loanswent to consumers with credit outside of prime, portends a vitaland healthy automotive market.”

Complete your profile to continue reading and get FREE access to CUTimes.com, part of your ALM digital membership.

Your access to unlimited CUTimes.com content isn’t changing.

Once you are an ALM digital member, you’ll receive:

- Critical CUTimes.com information including comprehensive product and service provider listings via the Marketplace Directory, CU Careers, resources from industry leaders, webcasts, and breaking news, analysis and more with our informative Newsletters.

- Exclusive discounts on ALM and CU Times events.

- Access to other award-winning ALM websites including Law.com and GlobeSt.com.

Already have an account? Sign In

© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.

link")