Some are calling it the strongest comeback to emerge from thedregs of the Great Recession.

|From the last year's drop in gasoline prices to a bevy of luresrolled out by manufacturers to woo shoppers, the auto industry ison track to post its highest volume since the year before theeconomy took a turn for the worse in 2008.

|Sales growth are in the double digits, with domestic car andtruck sales increasing 25% since 2011, according to Auto NationInc., which tracked activity through June 2012. The sale of importsskyrocketed 56%, with more than 11,500 cars and trucks sold in Junealone.

|Indeed, major automakers are basking in the surge. Toyota MotorCorp. recently reported a 60% increase in sales in the UnitedStates between June 2011 and June 2012. Good news for the thirdlargest automaker, which had to halt or significantly delayproduction last year following a destructive earthquake and tsunamiin Japan in March 2011.

|Automakers based in the U.S. are also on a sales high. In June,Chrysler was among the leaders with a 20% increase in salesfollowed by General Motors at 16% and Ford up 7%.

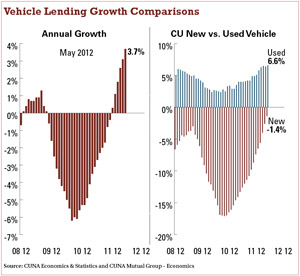

|For credit unions, the resurgence has helped to grow auto loan portfolios, particularly on the used vehicleside. Many have said they are in a more competitive position ascredit union loan rates continue to fall, according to CUNA MutualGroup's latest “Credit Union Trends Report.” As of April, theindustry experienced a 2.3% gain in auto loans, the best postingsince 2009 with $1.1 billion of the $3.9 billion annual gaindirectly tied to growth occurring this year.

|“What's behind all of this is more people are buying and carsare cheaper to buy now,” said Robert O'Hara, president ofcuautocoupon Inc., a Hauppauge, N.Y.-based provider of discountsand refinancing incentives to members at more than 20 creditunions.

|“The rebound seems to always be there for autos when the economygoes in the tank, for lack of a better phrase,” O'Hara said. “It'susually the first to go out and the first to come back.”

|That revival has also brought out more aggressive competitionwith dealers touting 0% financing on new cars in a race to latch onto eager shoppers.

|

“We've had to adjust our strategy a bit. We're seeing thegreatest interest on used autos,” said Teri Rapp, chief creditofficer at the $1.2 billion NuVision Credit Union in Huntington Beach, Calif. “We'reoffering the same pricing on new and used for ourmembers.”

|The 0% financing has certainly changed the way NuVision iscourting potential buyers from continuing to adjust rates to carsale partnership promotions, which have proven to be successful. Agoal of $1.2 million was set for a May used car sale on the creditunion's property. NuVision surpassed that bringing in $1.7 millionand several new member relationships, Rapp said.

|In addition to partnering with Autoland Inc., a vehicle buyingCUSO in Chatsworth, Calif., and using traditional advertising,which has yielded many pre-approvals, NuVision has installed loankiosks in its branches so that members can apply online, connectwith a representative and get approved in one swoop.

|“We want to capture them before they go shopping,” Rappsaid.

|Another edge is taking the time to educate members on what'sreally behind that so-called tantalizing 0% deal.

|“When you start to educate them on what they're getting for thepricing adjustment and the adders, they can see the actual loanbalance,” Rapp said. “If you do a side by side comparison, we haverates as low as 1.99%.”

|Overall, NuVision's auto loan business is up 11% for new andused–a strong showing for the credit union, Rapp said. Direct loansaccounted for $87.2 million while indirect loans were at $48million as of July, she added.

|After pulling out a few years ago, NuVision revived its indirectlending activity in 2011. This time around, the credit union istaking it slow, monitoring it carefully, limiting the number ofdealers it works with and has established stricter criteria forindirect lenders. Rapp said the lowest FICO band score is around635, but NuVision is starting to evaluate if that's sturdy enoughto protect it from risk.

|As the auto market reshapes, members with higher credit scoreswill once again have the largest number of suitors. Unfortunately,the reality for some credit unions is they just won't be able tocompete with dealer financing when it comes to individuals with700-plus FICOs, said Eddie Nevarez, vice president of businessdevelopment at the National Auto Loan Network in Newport Beach,Calif., which counts more than a dozen credit unions among itsclients.

|“As of late, the trend that we see in the new car market is veryfierce competition in financing. We are hearing from our creditunion partners that they cannot compete with 0% to 1.9%financing,” Nevarez said.

|Still, credit unions can take advantage of recapturing thoseloans financed with the dealer in the 650 to 699 range and manyothers who may have been misplaced in a loan from the dealershipfor various reasons such as being a first-time buyer of havingmoderate credit, he offered.

|Nevarez said while there may be a slight rebound in theauto market, a true rally will depend on the housingmarket. In the four states hardest hit–Arizona,California, Nevada, and Florida–new auto registration is still onthe decline,

|“But the silver lining is in the auto refinance market in thesestates. We are seeing members with moderate to prime credit takingadvantage of low auto rates offered by creditunions,” Nevarez said.

|For some, the verdict on refinancing opportunities is mixed.O'Hara at cuautocoupon said many members don't know they canrefinance their auto loan, which potentially creates an opening forcredit unions to educate them. Rapp at NuVision said refinancingactivity has been slow at NuVision.

|The $1.8 billion Grow Financial Federal Credit Union in Tampa, Fla., recentlylaunched a promotion that pays members $300 at closing forrefinancing their auto loan with the financialinstitution.

|“In the past, refinancing has brought in strong numbers and ourturnaround on refinancing on new cars is good too,” said JasonMoss, senior vice president of delivery channels at Grow Financial.“We've received a lot of good feedback and we're really expecting alot of loans.”

|In June, the credit union brought in $20 million in new growthloans including auto loans, which added to Grow Financial's $524million consumer loan portfolio, Moss said. Despite the increasedcompetition and lower rates brought on by the auto market's U-turn,there is more room to grow.

|“We go back to competing on service,” Moss said. “We primarilysee most of our activity on used. I would say new is starting topick up as the economy turns around. Indirect has been very well–wehad record growth in the last two months.”

|The scenario was quite different in 2008 and 2009, the yearscommonly referred to as the Great Recession. Moss said GrowFinancial maintained a very conservative eye on auto loans aspeople stopped buying cars and lenders scaled backsignificantly.

|“What we're seeing now is the market is coming back,” Moss said.“More people are interested in the auto loans were offering and ingeneral, overall lending.”

|While credit unions may not be offering the lowest rates tohitch on to the momentum, the industry continues to see a drop. Theestimated national average credit union new vehicle loan rate of3.77% was down 78 basis points since April 2011 and the usedvehicle loan rate was down 72 basis points to 4.35%, according toCUNA Mutual's Trends Report. Those rates are far away from theaverage rate of 7% in 2010, O'Hara said.

|As of April, the new vehicle loan portfolio was down 3.5%year-over-year but still grew that month and in March. Usedvehicles continued to been a significant source of total creditunion loan growth with a 5.8% or $6 billion jump inApril.

|The most surprising discovery may be with indirect loans. Morethan 100% of the first-quarter gain in total vehicle loans wasattributable to increases in the indirect portfolio, the datashowed. Point-of-purchase financing is also poised to a keyingredient for growth.

|O'Hara said there may be other areas of opportunities for creditunions to take advantage of the auto market's resurgence. For one,the average car is now about 11 years old, so people will belooking to replace their vehicles. Others might want to downsizefrom larger models such as SUVs to hybrids to take advantage ofmileage savings. He's noticed an increase in Fiat sales over thelast few months, for instance.

|The one constant within the credit union industry is thestruggle to capture auto loans without offering the best rates,O'Hara said. Most financial institutions are sticking with A paper,are skittish about B and C paper and are completely avoidingsubprime.

|“There's a market for many credit unions to go into B paper.That's good risk,” O'Hara offered. “These are good members. You'vehad a history with them and they're stable. Some credit unionsdon't know they are in the market to buy.”

Complete your profile to continue reading and get FREE access to CUTimes.com, part of your ALM digital membership.

Your access to unlimited CUTimes.com content isn’t changing.

Once you are an ALM digital member, you’ll receive:

- Critical CUTimes.com information including comprehensive product and service provider listings via the Marketplace Directory, CU Careers, resources from industry leaders, webcasts, and breaking news, analysis and more with our informative Newsletters.

- Exclusive discounts on ALM and CU Times events.

- Access to other award-winning ALM websites including Law.com and GlobeSt.com.

Already have an account? Sign In

© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.

link")