Just four months ago, economists at the Mortgage Bankers Association were predicting 2026 would be a year of easing inflation, declining mortgage rates and a decent gain in mortgage originations.

Then came a lesson in geography and economics. The U.S. and Israel attacked Iran Feb. 28; in response, Iran closed off the Strait of Hormuz, and we have since learned that not only does a goodly portion of the world's oil flow through there, but that oil prices affect not only gasoline prices but many other parts of the economy here at home.

It's a small world, after all.

The MBA economics team's Feb. 17 forecast had predicted residential first mortgage originations would rise 8.1% to $2.22 trillion in 2026 as the year ended with the Consumer Price Index at 2.4% and the 30-year mortgage rates at 6.1%. Not dramatically great, but headed in the right direction.

In their latest forecast, dated May 15, the MBA predicted originations will rise 5.8% to $2.17 trillion in 2026 as the year ends with inflation rising to 2.9% and mortgage rates rising to 6.5%. Not dramatically bad, but headed in the wrong direction.

The MBA economics team's latest commentary, dated May 29, noted that the April inflation rate came in at 3.8% for April, leading it to revise its forecast to say inflation will peak above 4% this year "and remain elevated for the next year or so."

"The longer the war and disruption to oil production and shipping continue, the larger the negative impact on the global economy, as purchasing power for both consumers and businesses is reduced," they wrote. "One notable data point in April's CPI report was that the rate of inflation was higher than wage growth for the month. Consumers are losing purchasing power and this will be reflected in reduced demand."

The Bureau of Labor Statistics reported June 10 that inflation in May was 4.2%.

The latest data for credit unions was through March, so the slight improvements shown in recent data have a lesser chance of continuing.

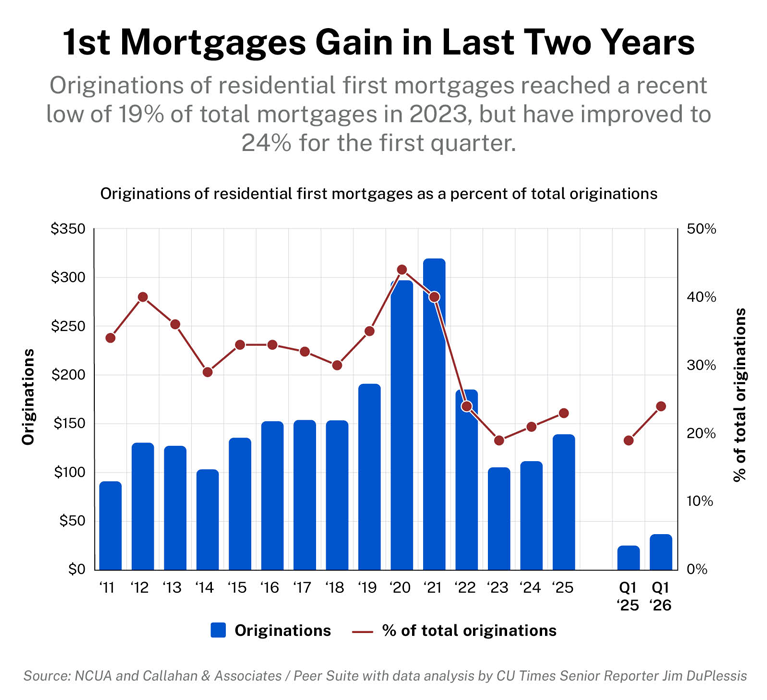

Credit unions originated first mortgages faster than the overall market in 2025 and the first three months of 2026.

This is based on a comparison of data from the MBA and NCUA, drawn from the Callahan Peer Suite.

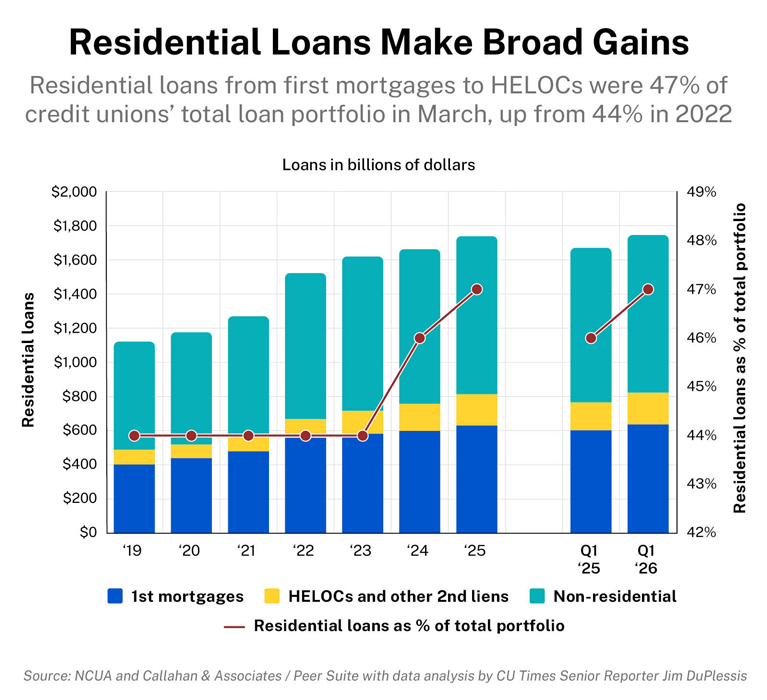

And first mortgages have become a larger portion of the credit union portfolio since 2023 – in large part because credit unions are losing share of auto loans.

The mortgage boom of 2020-2021 has been a boon and a curse.

For homeowners in the right position, they were able to refinance their homes at record low rates.

The MBA found 30-year fixed rates averaged 2.8% to 3.1% from March 2020 through the end of 2021.

Rates were 6.60% for the week ending June 5, but the MBA says they have been volatile because of the U.S. war against Iran.

With rates still high and perhaps getting higher, homebuying is increasingly unaffordable and the opportunities to refinance are narrow.

According to TruStage Chief Economist Steve Rick, the effective mortgage rate, which is the average rate on all outstanding mortgages, is almost 200 basis points below the current mortgage rate. "Following years of higher-than-average home price growth, the housing market appears overvalued. So, expect home price appreciation to slow to 0% to 1% in 2026," he wrote in a recent report.

While rates have often locked homeowners into homes that they have outgrown, the handcuffs are often golden.

With home prices continuing to rise, they are able to tap into that equity to meet other needs.

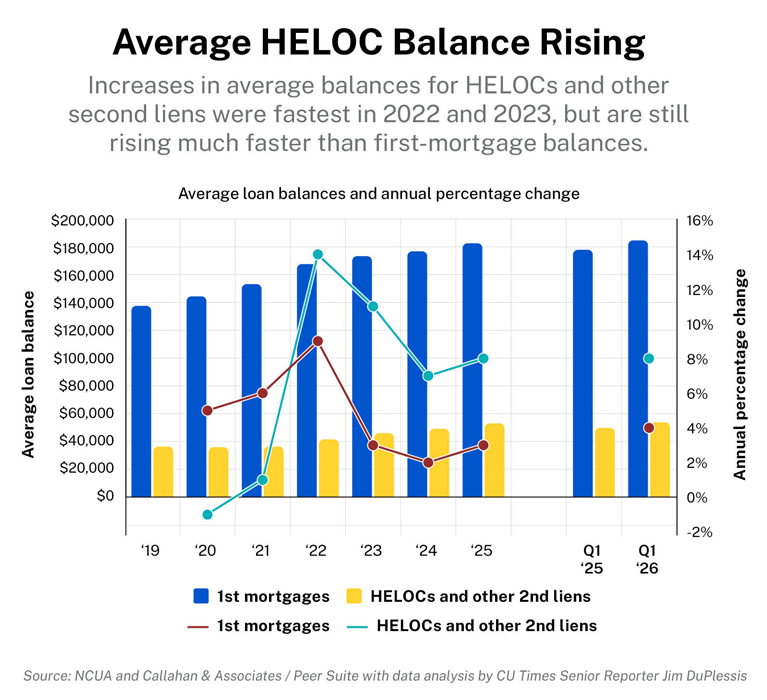

Home equity lines of credit and other second liens declined slightly at credit unions in 2020 and 2021, but exploded in 2023, rising 37%.

The rates of increase have fallen each year since, but HELOCs and other second liens still rose 15% last year and 14% in the first quarter compared with a year earlier.

HELOCs and other secondary liens grew from 16% of total residential loans in December 2022 to 23% in March 2026.

The NCUA doesn't report HELOCs separately from other second liens, but America's Credit Unions does.

AmCU estimates, which rely on Equifax data, show HELOCs ranged from 42% to 51% of the total second-lien residential loan category from July 2005 through March 2012. HELOCs have since risen steadily to account for 71% of second liens in March and April.

Homeowners' dependence on home equity also shows up in their average borrowing. The average balance for HELOCs and other second liens has grown from $36,544 in December 2021 to $53,981 in March.

The annual growth rates peaked at 14% in 2022, but second liens are still rising faster than first liens.

As of March, average balances for second liens had grown 8% from a year earlier, while the average first mortgage balance had risen only 4% to $182,994.

© Arc, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to TMSalesOperations@arc-network.com. For more information visit Asset & Logo Licensing.