Consumers are managing their cash flows with tools new and old. Besides the old-fashioned method of running up credit card debt in hard times, or skipping credit card payments, they are leaning into the newer ways, such as using person-to-person cash transfers and Buy Now, Pay Later (BNPL) programs.

Velera, the nation's largest payments CUSO, puts person-to-person apps like PayPal, crypto stuff and BNPL services into a category it calls "money services."

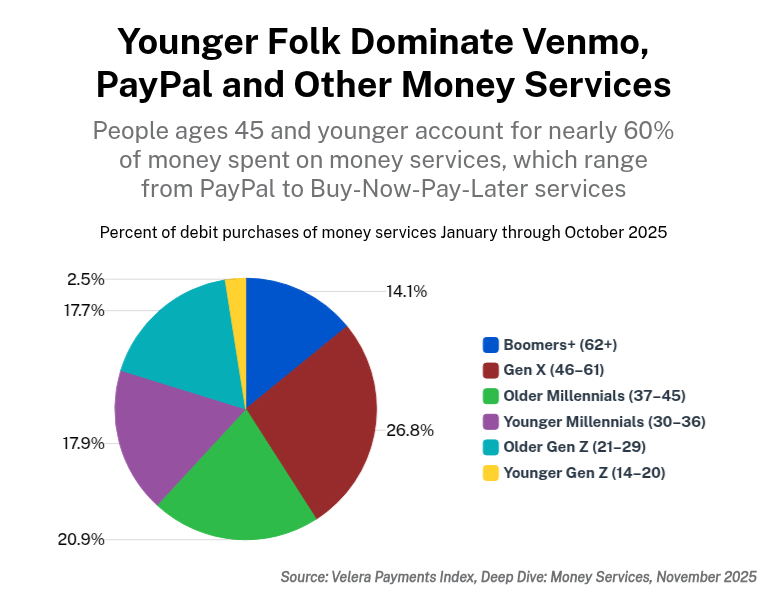

Money services account for only about 1% of credit card purchases, but more than 13% of debit card purchases, up from 3.8% in 2019.

Two-thirds of debit purchases for money services are for person-to-person apps.

Top merchants include Cash App, Venmo, Apple Cash, Remitly, Meta Pay and PayPal. Cash App and Venmo are the leading providers, but their share fell from 78.9% in 2024 to 76.3% this year.

A Velera "Deep Dive" report last November said an emerging trend within money services appears to be consumers adding to existing balances via debit purchases with traditional P2P vendors and fintech apps, such as Dave and Chime, which allow consumers to hold balances with them.

"Recently, the Consumer Financial Protection Bureau (CFPB) issued a consumer advisory reminding consumers that funds held in payments apps may not be insured by NCUA, FDIC or other insurers and should be moved to an account with deposit insurance," the Velera report said. "Beyond the CFPB advisory, consumers need to be aware of the limited support and customer service available with these tools. Minimal live support, the absence of fraud protection and the lack of transaction dispute processes should also be taken into consideration when using these apps."

Consumers ages 37 and older tend to use money services less often, but in greater amounts per transaction. They represent 56% of transactions and 62% of purchases.

The BNPL market has begun to mature.

In February, Velera looked at payments via cards to Affirm, Afterpay, Klarna, PayPal, Zip (formerly QuadPay), Sezzle, Sunbit and Flex Pay by Upgrade (formerly Uplift). It found total payments last year were 22% higher than in 2024, while the number of transactions grew only 12%.

The average BNPL payment increased from $39.04 in 2024 to $42.45 in 2025. Sunbit, which allows consumers to pay for auto repairs and medical expenses in installments, had a $122 average payment last year.

Affirm, Afterpay and Klarna represented approximately three-quarters of BNPL payments for 2025.

Zip and Sezzle had the highest cumulative growth in BNPL debit payments for 2025, up 56% and 51%, respectively.

Typically, short-term BNPL arrangements have four installments spread over six to eight weeks, whereas long-term plans can span six to 72 monthly installments.

According to PYMNTS Intelligence, consumers are no longer just using BNPL for holiday shopping surges, but to even out their cash flow throughout the year.

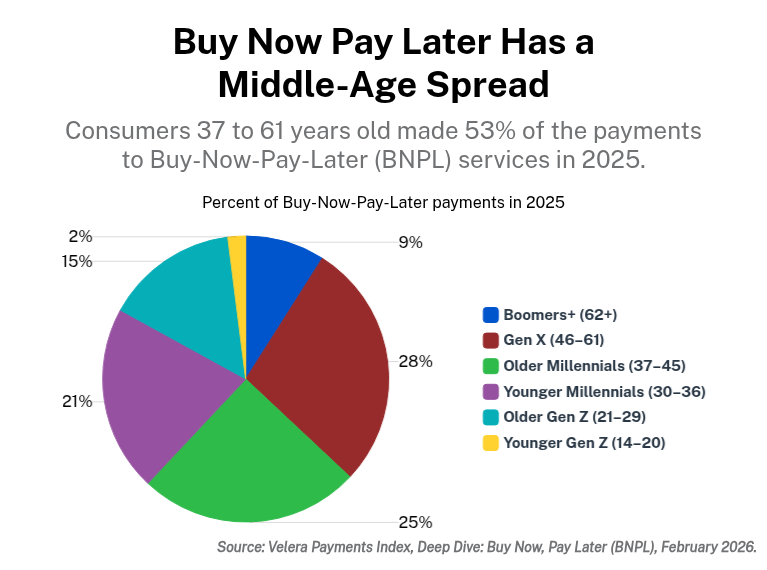

People ages 37 to 61 made more than half (53%) of BNPL payments last year.

Younger millennials (30-36) made 21% of purchases, and older Gen Z (21-29) made 15%.

In this K-shaped economy, a broad swath of Americans fly financially at tree-top level.

Velera's March "Deep Dive" reported that credit card delinquencies are rising, showing consumers are clipping tree tops more often.

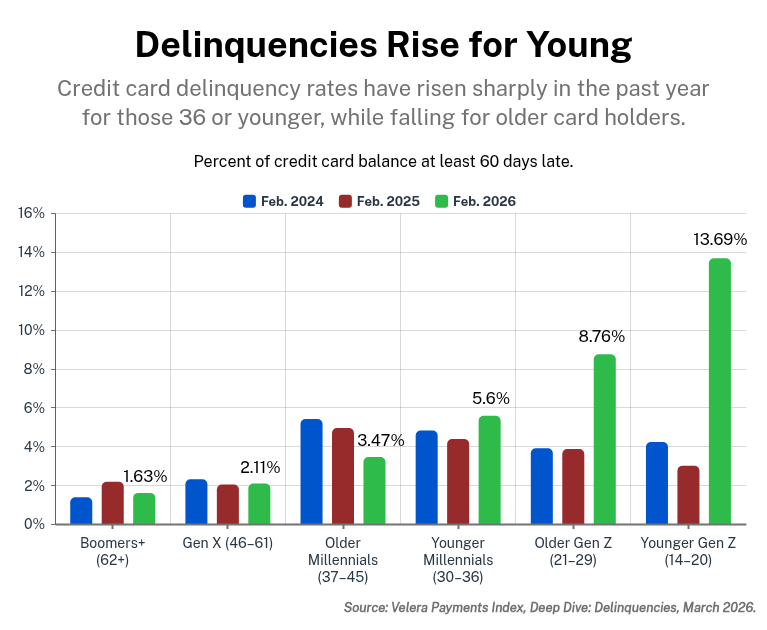

The overall credit card delinquency rate for February 2026 – defined as credit card balances two or more cycles past due as a share of total credit card balances – was 2.66% up from 2.49% in February 2025.

"This month's performance was consistent with the upward trend in year-over-year delinquency rate growth observed over the last four months, in contrast with the previous 10 months."

The findings by the Sherlocks at Velera included:

"Delinquency rates are higher for segments with lower estimated income and trend lower as estimated income increases."

"Delinquency rates tend to decline as the population ages." Those 62 and older had the lowest delinquency rate for February 2026 at 1.63%, while the Younger Gen Z (ages 14-20) had the highest rate at 13.69%. The Older Gen Z (ages 21-29) had the second-highest delinquency rate at 8.76%.

© Arc, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to TMSalesOperations@arc-network.com. For more information visit Asset & Logo Licensing.