Cars For Sale Stock Lot Row. Car Dealer Inventory. Photo: by Mikbiz/Shutterstock

Cars For Sale Stock Lot Row. Car Dealer Inventory. Photo: by Mikbiz/Shutterstock

As credit unions continued to slowly gain share in credit cards last summer, they continued losing share in the nation’s auto loan portfolio.

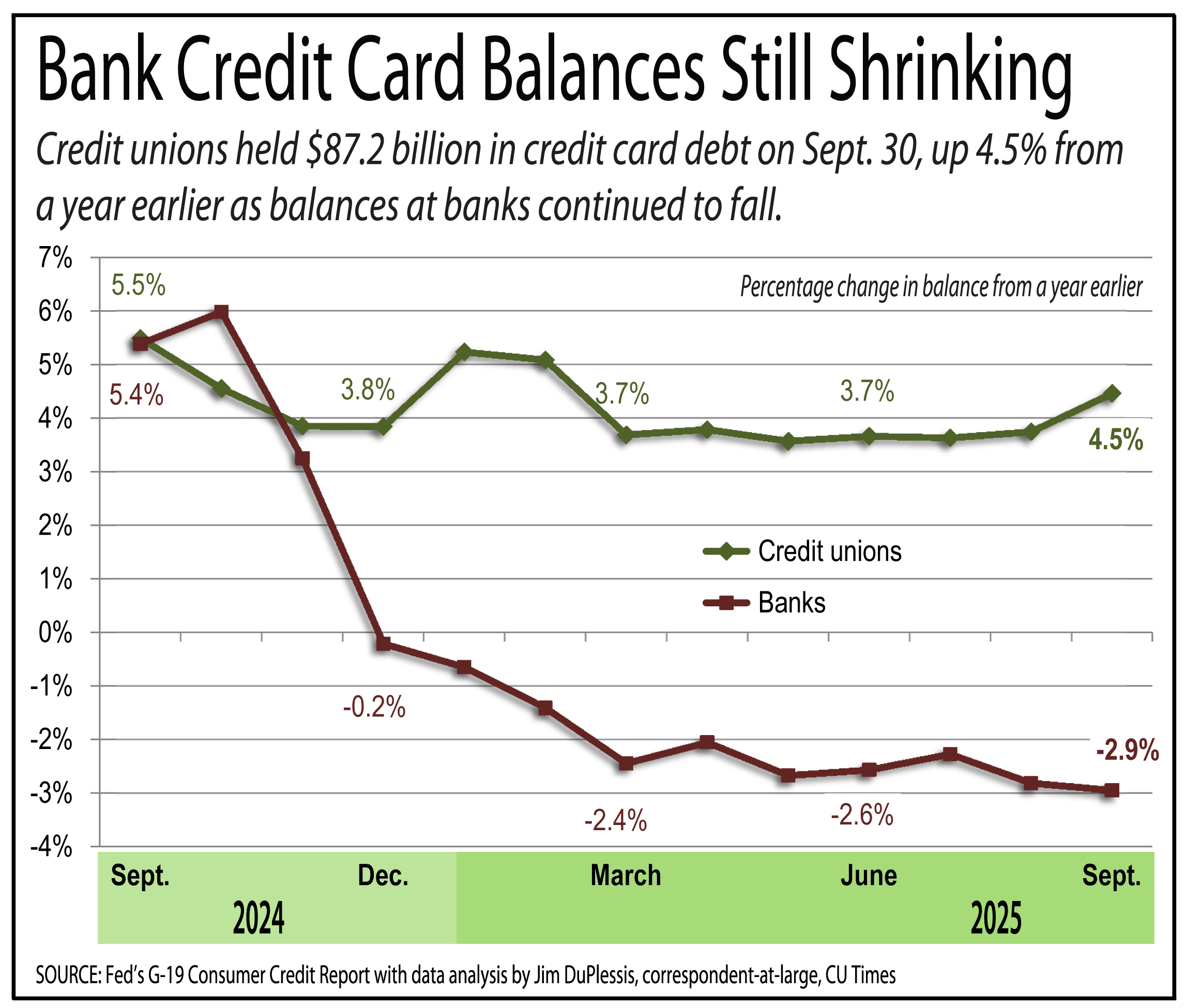

The Federal Reserve’s G-19 Consumer Credit Report released Friday showed credit unions held $87.2 billion in credit card debt, up 4.5% from a year earlier.

The credit card balance grew 0.8% from August to September, compared with an average August-to-September gain of 0.3% from 2015 through 2024. Credit unions’ share was 6.9% in September, compared with 6.8% in August and 6.4% in September 2024.

On quarter-ending months the G-19 includes balances for motor vehicle loans among all lenders.

The G-19 showed all lenders held $1.57 trillion in car loans in September, up 0.3% from a year earlier and up 0.4% from June.

NCUA data has been showing auto loan balances slipping for the past two years, and preliminary NCUA data from Callahan showed that trend continued in the third quarter.

Callahan’s Peer Suite had tallied third-quarter NCUA Call Reports from 4,392 credit unions as of Tuesday, representing 99.6% of the movement’s total assets.

The preliminary data showed credit unions held $486 billion in auto loans as of Sept. 30, down 0.9% from a year earlier and down 0.4% from June 30. One hopeful sign was the 12-month drops have been getting smaller since the end of 2024, when balances were down 3.2%.

After subtracting credit union loans from the total reported in the Fed’s G-19 report, auto loans held by others rose 0.9% from a year earlier and rose 0.8% from June 30.

The preliminary numbers showed credit unions’ share of auto loans at 31.0% on Sept. 30, down from 31.4% a year earlier and 31.3% in June.

Based on the assets of the credit unions not yet reporting, credit unions might have held $487.8 billion in auto loans, giving them a share of 31.1%. The balance would reflect a drop of 0.6% from a year earlier and no change from June.

Credit unions also fared better than banks in the G-19’s non-revolving consumer loans category, which includes auto loans, boat loans and personal loans.

Credit unions held $641.4 billion in non-revolving consumer loans in September, up 12.8% from a year earlier. The change was 0.4% from August to September, compared with the 10-year average gain of 0.7%.

Banks held $835 billion in non-revolving consumer loans in September, down 6.9% from a year earlier. The change was 0.9% from August to September, compared with the 10-year average gain of 0.6%.

Meanwhile, the Fed revised the 12-month change through August for credit card balances downward by 30 basis points for credit unions and 50 basis points for banks.

Banks held $1.2 trillion in credit card debt on Sept. 30, down 2.9% from a year earlier. The balance fell 0.6% from August to September, compared with a 10-year average of essentially no change. Banks’ share was 91.9% in September, compared with 91.9% in August and 92.2% in September 2024.

Finance companies held $15.6 billion in credit card debt in September, down 14.7% from a year earlier. The balance fell 1.44% from August to September, compared with the 10-year average gain of 0.8%.

The 10 credit unions with the largest credit card balances held $43.2 billion in credit cards as of Sept. 30 with an average balance of $5,315, a 60-day-plus delinquency rate of 2.49% and a use rate of 33.6%.

The 2,869 others with cards held $43.1 billion in credit cards as of Sept. 30 with an average balance of $2,446, a 60-day-plus delinquency rate of 1.57% and a use rate of 24.5%.

The Top 10 credit card holders at Sept. 30 were:

- Navy Federal of Vienna, Va. ($194.18 billion in assets, 15 million members) held $32.4 billion in credit cards as of Sept. 30 with an average balance of $6,518, a delinquency rate of 2.59% and a use rate of 37.1%.

- PenFed of Tysons, Va. ($29.35 billion in assets, 2.8 million members) held $1.8 billion in credit cards as of Sept. 30 with an average balance of $2,468, a delinquency rate of 3.07% and a use rate of 19.4%.

- BECU of Tukwila, Wash. ($28.9 billion in assets, 1.5 million members) held $1.7 billion in credit cards as of Sept. 30 with an average balance of $4,515, a delinquency rate of 1.48% and a use rate of 24%.

- SchoolsFirst FCU of Santa Ana, Calif. ($34.41 billion in assets, 1.5 million members) held $1.4 billion in credit cards as of Sept. 30 with an average balance of $3,733, a delinquency rate of 2.77% and a use rate of 30.1%.

- State Employees’ CU of Raleigh, N.C. ($56.79 billion in assets, 3 million members) held $1.2 billion in credit cards as of Sept. 30 with an average balance of $3,519, a delinquency rate of 1.78% and a use rate of 32.2%.

- Suncoast CU of Tampa, Fla. ($19.06 billion in assets, 1.3 million members) held $1.1 billion in credit cards as of Sept. 30 with an average balance of $3,888, a delinquency rate of 2.73% and a use rate of 30.4%.

- Mountain America FCU of Salt Lake City ($21.75 billion in assets, 1.4 million members) held $1.1 billion in credit cards as of Sept. 30 with an average balance of $2,381, a delinquency rate of 2.43% and a use rate of 31%.

- America First FCU of Riverdale, Utah ($23.32 billion in assets, 1.5 million members) held $999.9 million in credit cards as of Sept. 30 with an average balance of $3,683, a delinquency rate of 1.38% and a use rate of 25.5%.

- Pennsylvania State Employees CU of Harrisburg, Pa. ($9 billion in assets, 563,709 members) held $784.6 million in credit cards as of Sept. 30 with an average balance of $5,159, a delinquency rate of 1.2% and a use rate of 29.1%.

- Golden 1 CU of Sacramento, CA ($21.08 billion in assets, 1.2 million members) held $737.8 million in credit cards as of Sept. 30 with an average balance of $4,155, a delinquency rate of 2.45% and a use rate of 27%.

© Arc, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to TMSalesOperations@arc-network.com. For more information visit Asset & Logo Licensing.